They Are Preparing for a Different World

Sangram Datta

Sangram Datta

Every few months, headlines proclaim that the era of the US dollar is coming to an end. Whether it is a BRICS summit, an oil deal settled in a different currency, or another bilateral agreement bypassing the greenback, the same conclusion is often drawn: the dollar’s dominance is collapsing.

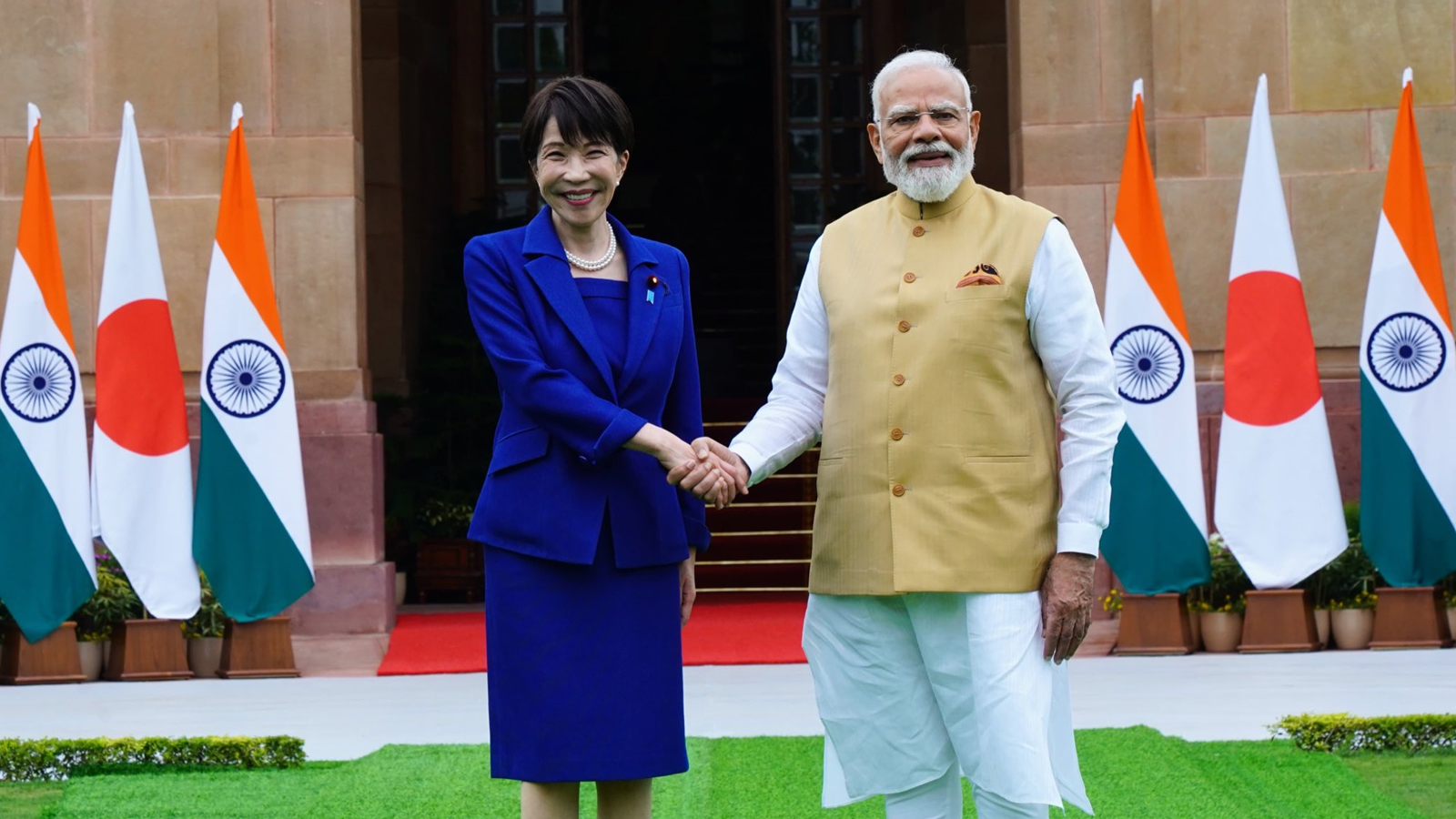

The latest discussion has been triggered by reports that India and Japan are exploring a framework that would allow parts of their bilateral trade to be settled directly in Indian rupees and Japanese yen rather than through the US dollar.

For many observers, this appears to be another chapter in the global “de-dollarisation” movement. It is a tempting narrative. It is also an oversimplification.

What is unfolding between India and Japan is less a rebellion against the existing financial order than a pragmatic attempt to make trade more efficient while adapting to a world that has become more economically fragmented and geopolitically uncertain.

The distinction matters.

For decades, the US dollar has occupied an unparalleled position in the international financial system. Around the world, central banks hold the majority of their foreign exchange reserves in dollars. Commodities from oil to wheat are largely priced in dollars. International loans, insurance contracts and cross-border investments continue to rely heavily on America’s currency.

That position is not simply a product of political influence. It reflects the depth of US financial markets, the liquidity of dollar-denominated assets, the rule of law underpinning those markets, and decades of confidence among investors and governments alike.

Replacing such a system is not something that happens because two countries sign a bilateral agreement.

Yet recent years have exposed vulnerabilities associated with relying too heavily on a single reserve currency.

The COVID-19 pandemic disrupted global supply chains. Russia’s invasion of Ukraine intensified geopolitical tensions and expanded the use of financial sanctions. Rising US interest rates strengthened the dollar while placing additional pressure on emerging market currencies. Businesses around the world became increasingly aware that exchange-rate volatility and dependence on intermediary currencies carry real financial costs.

Against this backdrop, many countries have begun exploring mechanisms that reduce unnecessary exposure to the dollar—not because they reject the existing order, but because they seek greater resilience within it.

India and Japan fit squarely into this trend.

The proposed Local Currency Settlement framework would allow designated transactions to be settled directly in rupees or yen. An Indian importer purchasing Japanese machinery, for example, would no longer necessarily have to convert rupees into dollars before payment. Likewise, Japanese firms investing in India could potentially conduct portions of those transactions without first acquiring large quantities of US currency.

The economic logic is straightforward.

Each additional currency conversion introduces transaction costs, exchange-rate risk and administrative complexity. Eliminating one layer of conversion can improve efficiency, particularly as bilateral trade and investment continue to expand.

For Japan, the timing is especially significant.

The Japanese yen has experienced one of its weakest periods in decades. Despite policy adjustments by the Bank of Japan and interventions in currency markets, the yen has remained under sustained pressure against the dollar. Reducing unnecessary demand for dollars in bilateral transactions therefore offers an economically rational response to an increasingly challenging monetary environment.

India has its own motivations.

New Delhi has spent several years cautiously promoting the international use of the rupee. The Reserve Bank of India has already established local currency settlement arrangements with partners including the United Arab Emirates, Indonesia and the Maldives. A similar framework with Japan would represent another incremental step rather than a revolutionary departure from existing policy.

However, limiting this story to currency settlement alone would miss the broader strategic picture.

India and Japan are steadily constructing one of Asia’s most consequential strategic partnerships.

Japanese investment has become central to India’s infrastructure ambitions, from industrial corridors to metro systems and the Mumbai-Ahmedabad high-speed rail project. Tokyo has repeatedly identified India as a critical destination for long-term manufacturing diversification at a time when companies are seeking alternatives to excessive dependence on a single production base.

Send your resume:

biswa@jigyasu.co.in

krcfoundation@gmail.com

Security cooperation has expanded alongside economic ties.

The two countries have strengthened naval exercises, deepened intelligence cooperation and increased defence collaboration through the Quad partnership with the United States and Australia. Recent discussions surrounding Japan’s Mogami-class stealth frigates further illustrate how industrial cooperation and defence policy are becoming increasingly intertwined.

Should multiple Indo-Pacific partners eventually operate similar naval platforms, interoperability would improve significantly. Maintenance, spare parts, logistics and joint operational planning could all become more efficient.

This is not merely about selling military equipment. It is about building long-term strategic ecosystems.

That broader geopolitical context also helps explain why local currency settlement matters beyond trade statistics.

Major infrastructure projects and defence cooperation involve billions of dollars over many years. Conducting portions of these financial flows in domestic currencies can reduce costs while making investment decisions less vulnerable to fluctuations in the dollar exchange rate.

None of this, however, should be mistaken for evidence that the dollar’s supremacy is about to disappear.

The greatest obstacle to any alternative currency is not politics but confidence.

International businesses choose currencies that offer stability, deep financial markets, predictable regulation and abundant liquidity. Governments can encourage local currency trade, but they cannot compel private firms to abandon the instruments they consider safest.

This remains India’s central challenge.

Although the rupee’s international profile has grown modestly, it is not yet widely held as a reserve asset. Investors remain cautious about long-term currency depreciation, capital controls and market depth. Expanding bilateral settlement frameworks is therefore only one piece of a much larger puzzle.

Ultimately, currencies derive international influence from economic fundamentals.

A currency becomes globally desirable when the world wants the goods, technologies and services produced by the economy behind it. Germany’s manufacturing, Japan’s industrial excellence, Switzerland’s financial credibility and America’s technological leadership have all reinforced confidence in their respective financial systems.

For India, the long-term objective cannot simply be increasing the number of countries willing to settle trade in rupees. It must be strengthening the industrial and technological foundations that naturally generate international demand for its currency.

That means expanding advanced manufacturing, semiconductors, defence exports, digital technologies, pharmaceuticals and high-value engineering.

Currency internationalisation is the consequence of economic transformation—not its starting point.

Perhaps the most important lesson from the emerging India-Japan partnership is that today’s international order is becoming increasingly multipolar without necessarily becoming anti-Western.

Japan remains one of America’s closest treaty allies. India continues to deepen strategic cooperation with Washington while simultaneously pursuing greater economic autonomy. These positions are not contradictory. They reflect the realities of a world where countries increasingly diversify relationships rather than choose exclusive blocs.

The future of global finance is therefore unlikely to be characterised by the sudden collapse of the dollar. A far more plausible outcome is the gradual emergence of a more diversified monetary landscape in which regional currencies play larger roles alongside—not instead of—the world’s dominant reserve currency.

Whether the India-Japan initiative ultimately succeeds will depend less on diplomatic announcements than on commercial behaviour. Governments may establish the framework, but markets will determine its relevance.

If businesses embrace rupee-yen settlements because they are cheaper, faster and more efficient, the agreement could become a significant milestone in the evolution of international finance. If not, it will remain another well-intentioned policy with limited practical impact.

Either way, the story is larger than the dollar itself.

It is about how middle powers are quietly redesigning the rules of economic cooperation for an era defined not by ideological confrontation, but by strategic flexibility, supply-chain resilience and national interest. In that changing world, the most significant revolutions are often the ones that arrive without declaring themselves revolutions at all.